Not too long ago, Brazil was an emerging markets champion. A decade of improved macroeconomic performance and stability in Brazilian policymaking, coupled with poor sentiment in developed markets following the global financial crisis, made investing in Brazil a hot prospect. This positive environment was evidenced by a sharp increase in private equity fundraising, which reached a cyclical peak in 2011, and the establishment of local offices by major global PE firms like KKR, Apax Partners, and HIG Capital.

But fast forward four years and the picture looks very different. The sluggish global economy and a drop in demand for raw materials has weakened Brazil and placed downward pressure on the Real. The U.S. Federal Reserve’s tapering of bond purchases has created uncertainty across emerging markets, as liquidity is withdrawn from the global system. Moreover, improving economic conditions in the U.S. has reduced investor’s willingness to tolerate risk in exchange for higher yielding emerging market investments. Add to this Brazilian government interventions in energy, electricity and financial sectors and the recipe for diminished investor confidence is complete.

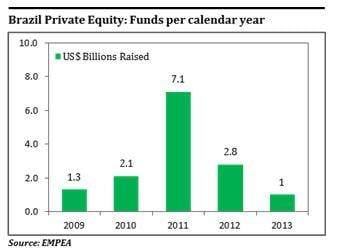

As we detail in our new report, Brazilian Private Equity: A New Direction, the market deterioration had a big knock-on effect on the private equity (PE) industry. At its peak in 2011, fundraising in Brazil reached a record US$7.1 billion, but dropped sharply in 2012 and 2013, as shown in the chart at right. The volatile environment also impacted both PE investment and exit activity, as PE firms and other investors struggled to adapt to the repricing of risky assets.

It’s getting harder

Deploying PE capital in the current environment has been a challenge. Deal activity in Brazil during 2013 reached its lowest since 2009 at US$2.8 billion, nearly 50 percent below its 2012 level. In addition to the increased political and macroeconomic risk outlined above, PE industry development during the cyclical upswing has exacerbated deal-making. The influx of international PE houses and dry powder resulting from 2010/11 fundraising has increased competition on a limited number of investment opportunities. With a market historically focused on growth capital investment in small and mid-sized investments, competition has been particularly pronounced at the larger end of the spectrum (deals in excess of US$100 million). In order to gain an edge in the competitive environment, proprietary deal sourcing and post-transaction value addition capability has become increasingly important.

Over the long-term, the structure of Brazilian financial markets presents additional headwinds for the PE industry. The lack of developed private debt markets continues to be a barrier for large leveraged buyouts, as 90 percent of the PE firms (general partners, or GPs) surveyed in our report said that the average deal employs leverage of 25 percent or less. Underdeveloped and volatile public equity markets limit access to the IPO market, placing a large emphasis on trade buyer and secondary PE buyer’s investment appetite. In addition, a historical lack of local limited partners (LPs) – those who invest in PE firms – in comparison to other emerging markets exposes Brazilian GPs to shifts in international investment flows.

“Cautiously optimistic”

While recent struggles and long-term structural impediments hamper the development of Brazil’s PE industry, the long-term trends that attracted investors to Brazil – positive demographics and a growing middle class – remain in place. Given what is viewed by some as the market’s recent shake-out, GPs surveyed for our report were cautiously optimistic about the industry’s prospects over the next three to five years.

GP respondents were particularly bullish about capital-intensive industries – such as infrastructure and oil & gas – and sectors like financial services and agribusiness were also viewed positively. In addition, as the middle class continues to grow, consumer spending on non-food goods, such as clothing and cellphones, and services, such as private education and healthcare, are also expected to provide further opportunities for investment.

The PE market outlook among LPs was more mixed. While international LPs see Brazil’s prospects as somewhat diminished compared to more recent bright spots in their portfolios, an increased PE allocation from several Brazilian LPs could bode well for domestic support of the industry moving forward.

Reflecting the latter trend, Brazilian pension funds PREVI and FUNCEF recently announced their intention to increase the share of PE investments in their portfolios. PREVI is expected to increase its PE allocation to from 0.6 percent to 2-3 percent in one of its funds and from 1.8 percent to 4-5 percent in another. FUNCEF announced its intention to increase its overall 12 percent commitment to 15 percent. These allocations compares favourably with the 10 percent allocation to the PE industry by large LPs such as CalPERS and the Ontario Teachers’ Pension Plan (“Teachers” as it’s commonly known). Although these investors still represent a small share of the industry’s investor base, they have size and potential to be a significant source of industry capital in the long run.

-

View Comments

(2) -

Shreekumar Rakshit

Brazil has some serious structural issues. Poor consumer financing will be a drag on consumer demand. Fiscal imbalances will always be a source of macro risk. Access to debt capital for SME's is difficult and the cost is also high. Lack of infrastructure will keep the cost of doing business high. Without improvements on these underlying issues, entrepreneurial activities may not pick up significantly. However, in such a context, PE firms can find some good deals in the SMEs which will need capital for growth, expertise for operational improvement and international expansions.

-

Leave a Comment

Related Reads

Economics & Finance

Where Are the Best Private Equity Returns?

Strategy

Private Equity vs. The Strategic Acquirer

Economics & Finance

Anonymous User

26/03/2015, 04.42 pm

Despite the accurate description of the economic environment in Brazil, I tend to disagree with using fundraising figures to explain its impact for PE in Brazil.

I think that it is important to mention here that record fundraising years in Brazilian PE (2010/2011) have been driven by a small pool of $1bn+ funds. They were in the market those years and they have come back in 2014 (some of them holding final closings in 2015). Since this was published in March 2015, you will notice that, according to LAVCA, Brazil-focused funds captured $5.6 billion over 23 funds in 2014.

All that said, I think fundraising activity is not a good predictor of appetite/interest in the case of Brazil. Additionally, pan regional funds raised in LatAm invested large portions of its capital in Brazil during the period 2012-2014, driving deal activity to record levels in 2012 and 2013, while a strong mid-market activity allowed LPs to look investment options beyond these large GPs. Other interesting development has been the presence of global funds investing in Brazil for the first time, like KKR and Bain Capital did last year.