According to the SME Finance Forum, 41 percent of formal micro, small and medium enterprises in emerging markets have unmet financing needs. This gap currently amounts to US$5 trillion or 1.3 times the current level of financing. If we only consider Southeast Asia, one of the most dynamic regions globally, this funding gap amounts to almost US$300 billion.

This lack of funds isn’t a niche problem because these firms are the core of the economy. According to a 2015 Deloitte study, SMEs contribute 42 percent of the combined GDP of the five founding members of ASEAN and largest Southeast Asian economies (Indonesia, Malaysia, Philippines, Singapore and Thailand).

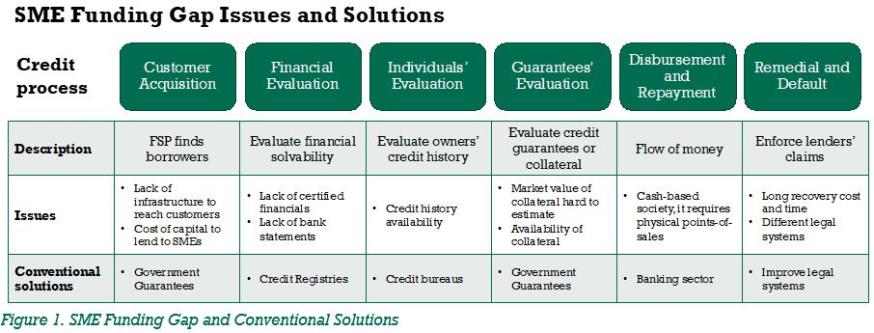

There are multiple reasons for the financing gap. Traditional financial services providers (FSP) have historically been unable to meet SME needs for several reasons, which include the difficulty in capturing and utilising financial information. In this domain, fintech can offer a major breakthrough. In Figure 1, we present an analytical framework itemising the main components of the lending process.

For SMEs, each step in the process represents a hurdle that common market solutions are not always able to surmount.

- The marginal cost of setting up physical bank branches to reach businesses in remote areas is considerably higher than the marginal benefit of acquiring such customers.

- There is a dearth of credible data on companies or individuals for the purpose of evaluating credit risk. Without this input, financial intermediaries have to rely on alternative sources of data, which are typically hard to verify.

- SMEs in emerging Southeast Asia are asked to provide personal guarantees or additional collateral to compensate for the lack of credit history or information. In addition, several countries also lack legal frameworks to enforce collateral seizing if necessary or collateral registries.

- According to a study from PayPal, cash is still king in much of Southeast Asia. In the Philippines, Thailand and Indonesia, it is used in at least 70 percent of all transactions. The lack of an extended network of bank branches is a limiting constraint as it prevents financial institutions from managing disbursement and repayment.

- A credit remedial and default legal framework plays a crucial role in any recovery that banks can expect in case of default. Southeast Asian countries have different and often conflicting legislation as it pertains to borrowers or creditors.

Traditional banking therefore is not serving SMEs, a vital and necessary part of the Southeast Asian economy.

Fintechs can narrow the SME funding gap

Financial technology (fintech) can play a crucial role in reducing the funding gap. The digitalisation of business, specifically in procurement, sales, payment and accounting, provides low-cost access to credible data, enabling trust and access to funding.

Inspired by the example of neighbouring China, Southeast Asian countries have made digitalisation a priority of their regional growth strategy. In the ASEAN ICT Masterplan 2020, member countries have made digitalisation a priority by promoting a digitally-enabled, secure, sustainable and transformative economy. Efforts by every state have made ASEAN the fastest growing Internet market in the world, with an estimated 125,000 new customers entering every day.

As SMEs increasingly utilise internet services to manage vital parts of their business, including relationships with their suppliers or customers, they become more accessible to other types of providers. In this context, fintech companies can access a growing base of potential borrowers.

As their business becomes digital, SMEs will inevitably create a high quantity of data. Innovative financial services providers can utilise those data to either improve the quality of credit risk management or develop a more targeted product offering.

Albeit new and still small compared to the traditional banking sector, fintech lending is here to stay. According to a report by Google, Temasek and Bain & Company, the digital loan book across the region amounted to US$23 billion in 2019. It is expected to grow at 29 percent CAGR until 2025, to US$110 billion.

The winning model of P2P lending

One exciting fintech business model is peer-to-peer lending (P2P). It allows for the direct matching of units short of funds with units in surplus of them. The P2P platform must assess credit risk and facilitate the matching of investors and borrowers, individuals or corporate firms.

A good example is Singapore’s Validus Capital, which offers working capital financing and short-term loans to credit-constrained SMEs using the peer-to-peer model. After borrowers request funding, Validus uses a proprietary algorithm to analyse the credit risk. Once borrowers are approved, investors can directly finance them. Because the entire transaction takes place on the platform, borrowers can follow their funding application status and investors can easily access information about their outstanding investments. The P2P lender operates in Singapore, Vietnam and Indonesia and has disbursed more than S$450 million. Validus and other fintech lenders that target SMEs, like eLoan in Vietnam or Alixco in Malaysia, are not out for traditional banking’s share of the market; they are interested in meeting the funding needs of an underserved and unbanked population.

Imperative need for efficient regulations

Credible fintech regulations are necessary to create trust, a fundamental requirement in attracting funding. In China, there were 3,500 P2P lending platforms in 2015. One year later, the Chinese Banking Regulatory Commission showed that 40 percent of those were, in effect, Ponzi schemes.

Southeast Asian countries have adopted different approaches in regulating the fintech sector before allowing it to extend credit. Thailand, for example, has decided to allow only authorised entities to lend and recently issued a regime for P2P lending. In Vietnam, by contrast, peer-to-peer players operate without oversight, leading to the proliferation of platforms and interest rates of up to 70 percent.

Regulatory oversight should aim to protect investors in P2P platforms from mismanagement, and borrowers from usurious interest rates and unacceptable recovery practices. With its flexible regulation and ease in attracting capital, Singapore is the fintech hub of Southeast Asia.

This article was based on an INSEAD MBA Independent Study Project, “Peer-to-peer SME lending in Southeast Asia”, by Nicolò Maneri, supervised by Professor Jean Dermine.

-

View Comments

-

Leave a Comment

Related Reads

Strategy

How Social Impact Start-ups Are Solving Brazil’s Covid-19 Challenges

Economics & Finance

How the Unbanked Can Save and Borrow

Economics & Finance

No comments yet.